China stock market experienced a rapid rise in the third quarter, and the money-making effect began to accumulate. In October, the Sino-US trade war became tense again, and the stock market entered a volatile period. But we think there is no need to worry. The bull market will continue to develop despite of some drawdowns.

Capital inflow potential is enormous. Excess bank term deposits of RMB8 trillion accumulated from 2022 to 2024 will mature by the end of 2026. Medium to long-term wealth management products mature at a rate of RMB700 billion per quarter. And Chinese insurance companies are required to allocate an additional RMB500 billion annually to stock investments. China was seen adapted and posed a better position in the Sino-US trade tension periods in April and October. As the competitive dynamics between China and the U.S. gradually become clearer, foreign investment’s demand for long-term allocation of Chinese assets will increase. These factors constitute the immense potential of capital inflows. There is plenty of money looking for investment opportunities.

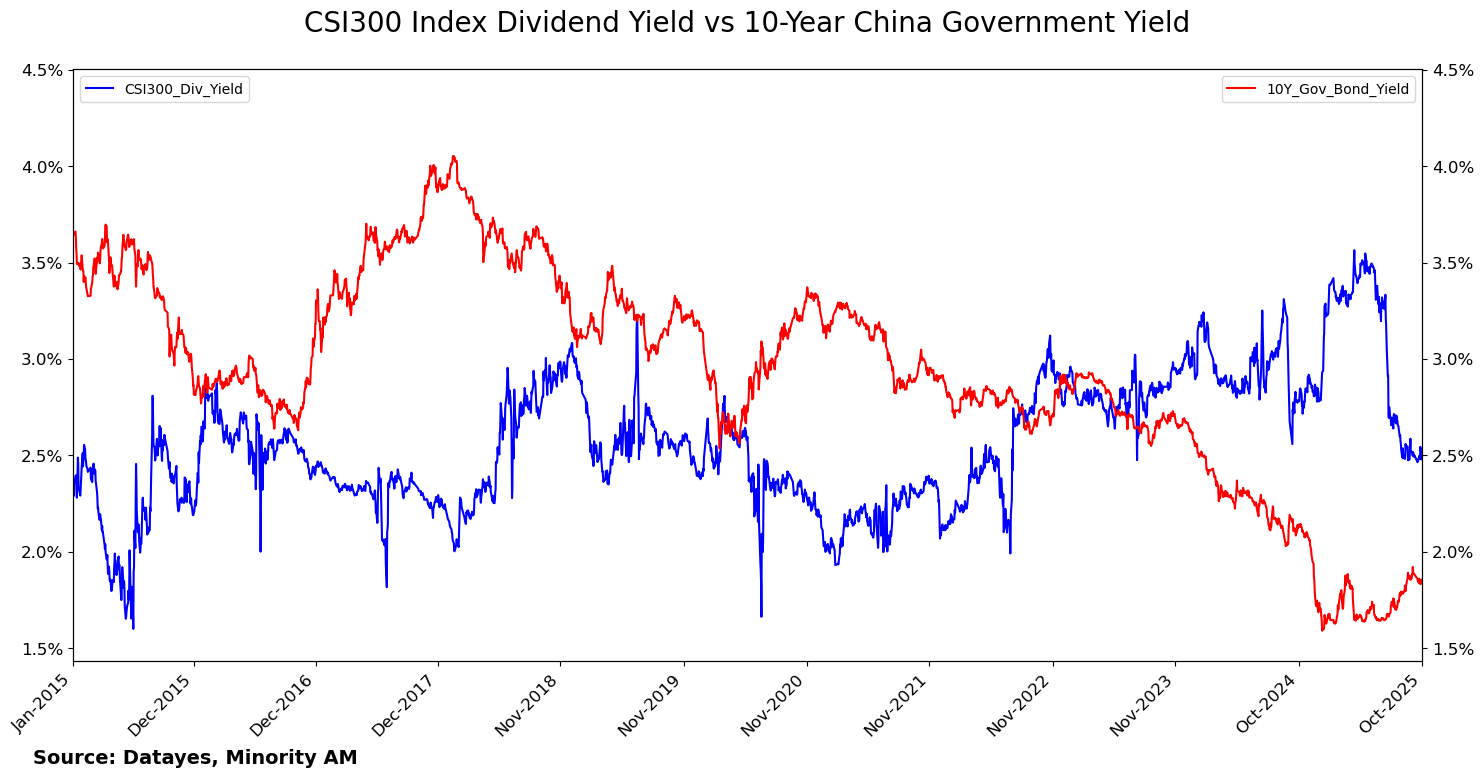

Stock market is highly attractive in a low-interest-rate environment. The yield on China's 10-year government bonds is 1.77%, whereas the average dividend yield of the CSI 300 Index is 2.5%, exceeding the government bond returns. Only 35% of the net profits of listed companies, on average, are distributed as dividends, with the majority of profits retained within the companies. The ratio of earnings per share to stock price for the CSI 300 Index constituents currently stands at 7.14%. In comparison, the annualized return on bank wealth management products is 1.5%, and the one-year deposit interest rate is 0.95%. The valuation of the Chinese stock market is very attractive.

The stock market is attracting capital inflow and is far from reaching its peak. Net inflow to mutual funds was RMB200 billion in September, totaling net inflow of RMB450 billion in 2025Q3. During the market peaks in 2015 and 2021, net inflow to mutual funds in a single quarter reached RMB750 billion. In contrast, the current market is far from such level. The market share of mutual funds is increasing while the scale of the stock market is expanding. We estimate that the market will approach the peak of the bull market when net inflow in a single quarter surpasses RMB750 billion.

What drives the bull market is the money-making effect. Retail investors, who are holding either stocks or mutual funds, are experiencing wealth increase, in turn, attracting new capital inflows. The CSI 300 Index and the ChiNext Index have surged by 16% and 38% respectively year to date. Mutual funds have generally achieved substantial profits, recouping losses from previous years. Investors’ sentiments are rapidly recovering.

The bull market is replacing the property market in creating a wealth effect. In the two decades before 2020, the property market was the main investment target and generated a wealth effect. Now, the property market is in a downward cycle, dragging China’s economic growth down. Meanwhile, the Sino-US trade war has exerted extra burden to the economy. At this moment, the bull stock market is able to cater investment needs and create a money-making effect. Both the transformation of economic structure and the formation of new productive forces take time, while a booming stock market may help to revive consumption and stabilize property market in short term.

Small-caps and growth stocks should weigh higher in a bull market. Historical data shows that small-caps and growth stocks took the largest gains during the 2013-2015 bull market. In the 2019-2021 bull market, growth stocks performed the best, while small-caps also gained significantly. This is not only supported by statistics but also aligns with investment intuition. Traditional large blue-chips have seen relatively smaller gains year to date, leaving room for catch-up. Although small-caps and growth stocks have already risen significantly this year, their risk-reward ratio still remains favorable. In a bull market environment, it is important to boldly allocate higher weight to small-caps and growth stocks.

Stock market is susceptible to macro-economic conditions and geopolitical issues. No one can predict when the market will adjust and how deep the contraction will be as they are influenced by future events. It is more important to maintain confidence in China's economic development and hold stocks patiently in a bull market. As long as the upward trend remains slow and unchanged, while the market sentiment does not overheat, future market adjustments actually provide good buy opportunities.